A2. Periodic LIFO

"Periodic" means that the Inventory account is not updated during the accounting period. Instead, the cost of merchandise purchased from suppliers is debited to an account called Purchases. At the end of the accounting year the Inventory account is adjusted to equal the cost of the merchandise that is unsold. The other costs of goods will be reported on the income statement as the cost of goods sold.

"LIFO" is an acronym for Last In, First Out. Under the LIFO cost flow assumption, the last (or recent) costs are the first ones to leave inventory and become the cost of goods sold on the income statement. The first (or oldest) costs will be reported as inventory on the balance sheet.

Remember that the costs can flow differently than the goods. In other words, if Corner Shelf Bookstore uses LIFO, the owner may sell the oldest (first) book to a customer, but can report the cost of goods sold of $90 (the last cost).

It's important to note that under LIFO periodic (not LIFO perpetual) we wait until the entire year is over before assigning the costs. Then we flow the year's last costs first, even if those goods arrived after the last sale of the year. For example, assume the last sale of the year at the Corner Shelf Bookstore occurred on December 27. Also assume that the store's last purchase of the year arrived on December 31. Under LIFO periodic, the cost of the book purchased on December 31 is sent to the cost of goods sold first, even though it's physically impossible for that book to be the one sold on December 27. (This reinforces our previous statement that the flow of costs does not have to correspond with the physical flow of units.)

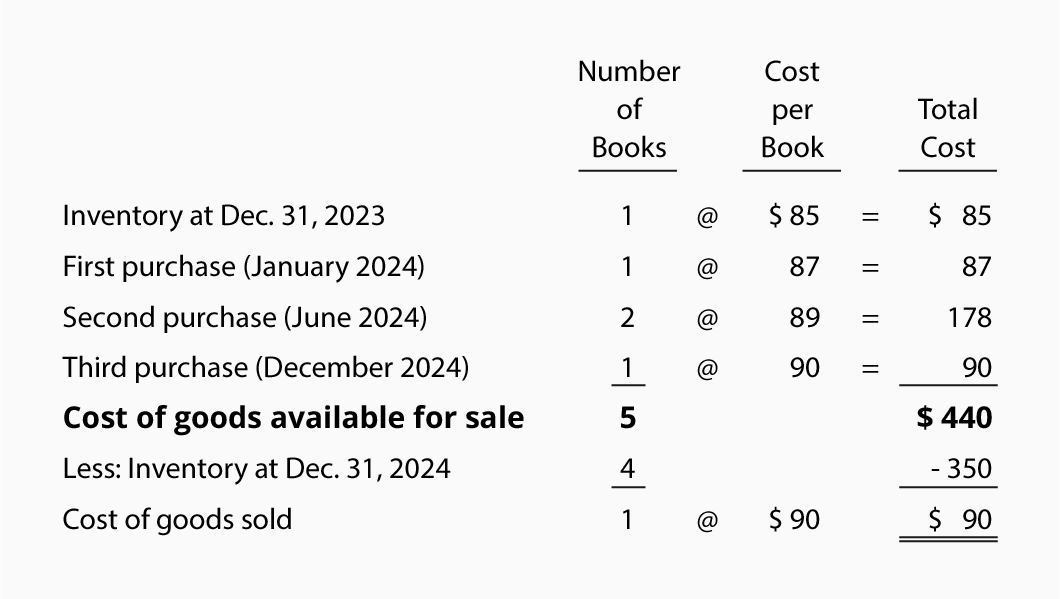

Let's illustrate periodic LIFO by using the data for the Corner Shelf Bookstore:

As before we need to account for the total goods available for sale: 5 books at a cost of $440. Under periodic LIFO we assign the last cost of $90 to the one book that was sold. (If two books were sold, $90 would be assigned to the first book and $89 to the second book.) The remaining $350 ($440 - $90) is assigned to inventory. The $350 of inventory cost consists of $85 + $87 + $89 + $89. The $90 assigned to the book that was sold is permanently gone from inventory.

If the bookstore sold the textbook for $110, its gross profit under periodic LIFO will be $20 ($110 - $90). If the costs of textbooks continue to increase, LIFO will always result in the least amount of profit. (The reason is that the last costs will always be higher than the first costs. Higher costs result in less profits and usually lower income taxes.)

A3. Periodic Average

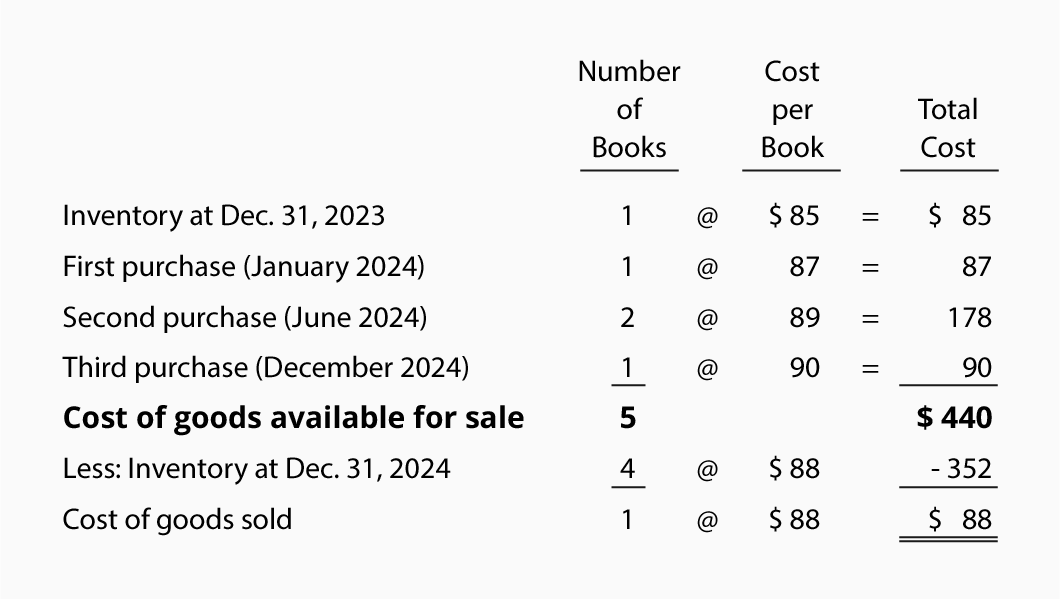

Under "periodic" the Inventory account is not updated and purchases of merchandise are recorded in an account called Purchases. Under this cost flow assumption an average cost is calculated using the total goods available for sale (cost from the beginning inventory plus the costs of all subsequent purchases made during the entire year). In other words, the periodic average cost is calculated after the year is over—after all the purchases of the year have occurred. This average cost is then applied to the units sold during the year as well as to the units in inventory at the end of the year.

As you can see, our facts remain the same-there are 5 books available for sale for the year 2011 and the cost of the goods available is $440. The weighted average cost of the books is $88 ($440 of cost of goods available ÷ 5 books available) and it is used for both the cost of goods sold and for the cost of the books in inventory.

Since the bookstore sold only one book, the cost of goods sold is $88 (1 x $88). The four books still on hand are reported at $352 (4 x $88) of cost in the Inventory account. The total of the cost of goods sold plus the cost of the inventory should equal the total cost of goods available ($88 + $352 = $440).

If Corner Shelf Bookstore sells the textbook for $110, its gross profit under the periodic average method will be $22 ($110 - $88). This gross profit is between the $25 computed under periodic FIFO and the $20 computed under periodic LIFO.

[source]

[source]

0 comments:

Speak up your mind

Tell us what you're thinking... !