Inventory Systems

Each of the three cost flow assumptions listed above can be used in either of two systems (or methods) of inventory:

A. Periodic

B. Perpetual

B. Perpetual

A. Periodic inventory system. Under this system the amount appearing in the Inventory account is not updated when purchases of merchandise are made from suppliers. Rather, the Inventory account is commonly updated or adjusted only once—at the end of the year. During the year the Inventory account will likely show only the cost of inventory at the end of the previous year.

Under the periodic inventory system, purchases of merchandise are recorded in one or more Purchases accounts. At the end of the year the Purchases account(s) are closed and the Inventory account is adjusted to equal the cost of the merchandise actually on hand at the end of the year. Under the periodic system there is no Cost of Goods Sold account to be updated when a sale of merchandise occurs.

In short, under the periodic inventory system there is no way to tell from the general ledger accounts the amount of inventory or the cost of goods sold.

B. Perpetual inventory system. Under this system the Inventory account is continuously updated. The Inventory account is increased with the cost of merchandise purchased from suppliers and it is reduced by the cost of merchandise that has been sold to customers. (The Purchases account(s) do not exist.)

Under the perpetual system there is a Cost of Goods Sold account that is debited at the time of each sale for the cost of the merchandise that was sold. Under the perpetual system a sale of merchandise will result in two journal entries: one to record the sale and the cash or accounts receivable, and one to reduce inventory and to increase cost of goods sold.

Inventory Systems and Cost Flows Combined

The combination of the three cost flow assumptions and the two inventory systems results in six available options when accounting for the cost of inventory and calculating the cost of goods sold:

A1. Periodic FIFO

A2. Periodic LIFO

A3. Periodic Average

B1. Perpetual FIFO

B2. Perpetual LIFO

B3. Perpetual Average

A2. Periodic LIFO

A3. Periodic Average

B1. Perpetual FIFO

B2. Perpetual LIFO

B3. Perpetual Average

A1. Periodic FIFO

"Periodic" means that the Inventory account is not routinely updated during the accounting period. Instead, the cost of merchandise purchased from suppliers is debited to an account called Purchases. At the end of the accounting year the Inventory account is adjusted to equal the cost of the merchandise that has not been sold. The cost of goods sold that will be reported on the income statement will be computed by taking the cost of the goods purchased and subtracting the increase in inventory (or adding the decrease in inventory).

"FIFO" is an acronym for First In, First Out. Under the FIFO cost flow assumption, the first (oldest) costs are the first ones to leave inventory and become the cost of goods sold on the income statement. The last (or recent) costs will be reported as inventory on the balance sheet.

Remember that the costs can flow differently than the goods. If the Corner Shelf Bookstore uses FIFO, the owner may sell the newest book to a customer, but is allowed to report the cost of goods sold as $85 (the first, oldest cost).

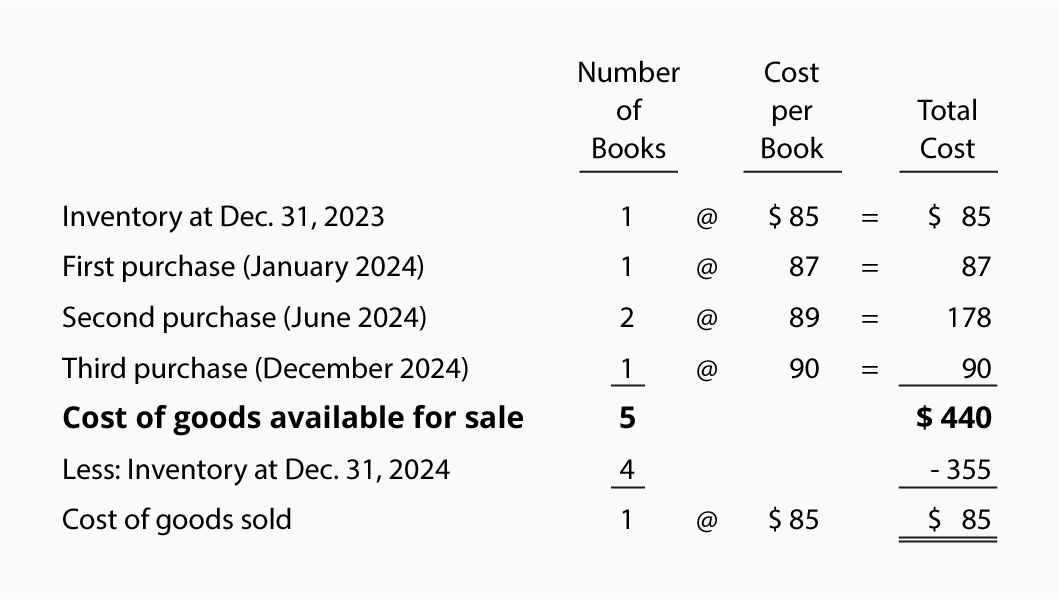

Let's illustrate periodic FIFO with the amounts from the Corner Shelf Bookstore:

As before, we need to account for the total goods available for sale (5 books at a cost of $440). Under FIFO we assign the first cost of $85 to the one book that was sold. The remaining $355 ($440 - $85) is assigned to inventory. The $355 of inventory costs consists of $87 + $89 + $89 + $90. The $85 cost assigned to the book sold is permanently gone from inventory.

If Corner Shelf Bookstore sells the textbook for $110, its gross profit under periodic FIFO will be $25 ($110 - $85). If the costs of textbooks continue to increase, FIFO will always result in more profit than other cost flows, because the first cost is always lower.

[source]

[source]

0 comments:

Speak up your mind

Tell us what you're thinking... !